Real-time weather data provides a live feed of atmospheric and environmental information, capturing precise conditions as they unfold. For decision-makers in commercial insurance and climate risk management, this capability is the difference between reacting to a crisis and proactively managing it. This is no longer a competitive advantage; it is a strategic imperative for profitability and operational resilience.

Frankly, relying on historical models in an era of increasing climate volatility is a significant business liability.

Why Real Time Weather Data Is a Strategic Imperative

Historical data shows past events, but it is blind to the dynamic, high-velocity weather threats of today. Real time weather data bridges this critical gap by providing a live view of evolving risks, directly impacting core functions from underwriting and risk selection to claims processing and portfolio management.

This immediate awareness enables underwriters to price policies with greater precision, reflecting an asset's true, current exposure. For risk managers, it opens a crucial window to deploy loss prevention strategies *before* an event occurs. Alerting a commercial client to secure a construction site hours before a high-wind event fundamentally shifts the business model from paying for losses to actively preventing or mitigating them.

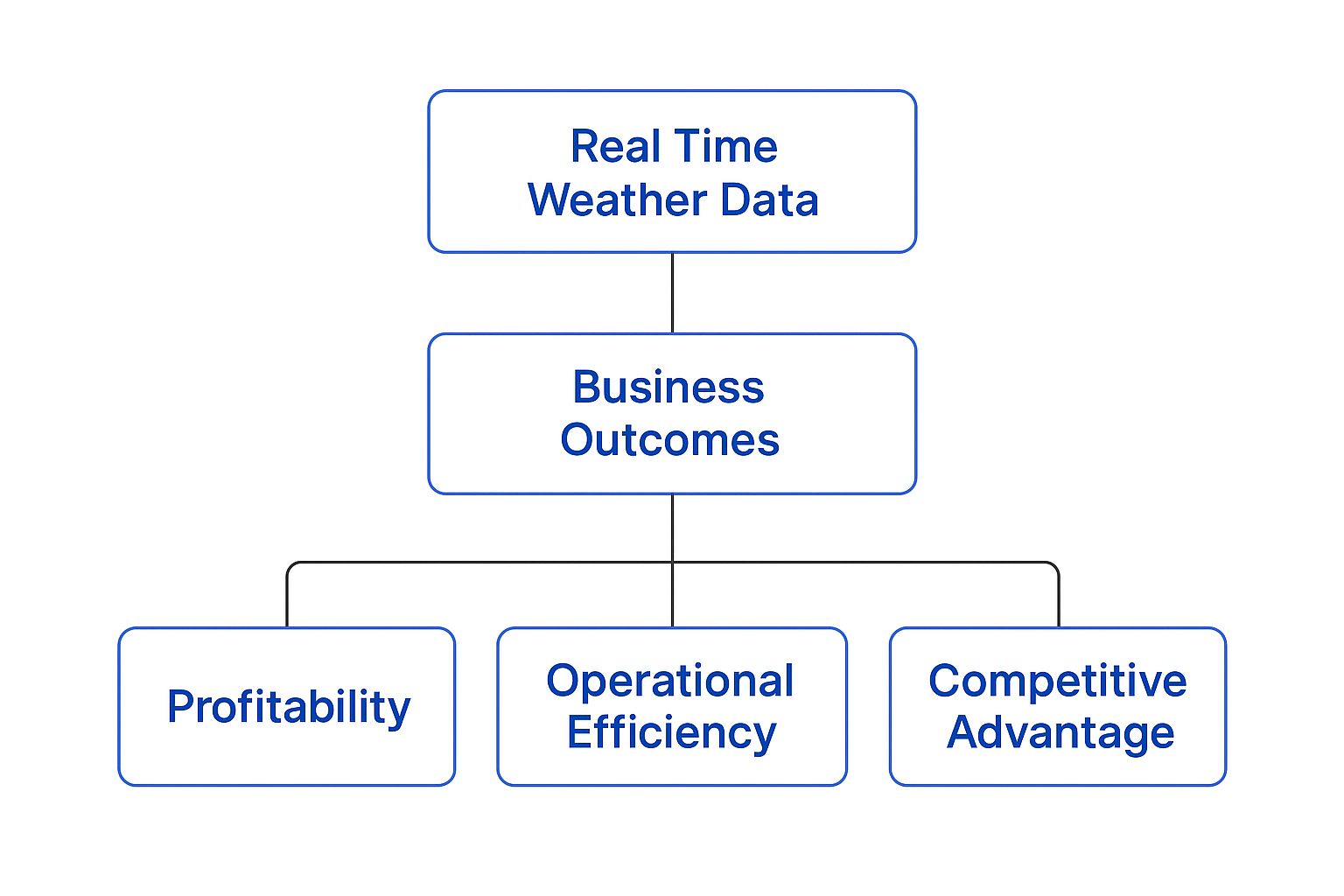

Redefining Business Outcomes

Integrating live weather feeds into core operations creates a distinct competitive edge by improving key performance indicators. This is not merely about better forecasting; it's about making business functions more intelligent and efficient. For decision-makers, this delivers tangible results across three primary areas:

- Profitability: More accurate underwriting reduces adverse selection, and data-driven claims validation minimizes fraudulent payouts, directly impacting the bottom line.

- Operational Efficiency: Automated alerts and data-driven workflows accelerate claims validation, reduce manual intervention, and lower loss adjustment expenses (LAE).

- Competitive Advantage: Offering proactive, risk-mitigation services to clients builds loyalty, improves retention, and establishes market leadership.

This diagram shows how real-time data is the foundation for achieving these critical business goals.

Infographic about real time weather data

As the visual clarifies, mastering live data is the starting point for enhancing profitability, efficiency, and market position. The value of immediate insights extends beyond meteorology; parallels can be seen by exploring real-time data's impact on business operations in other sectors.

Ultimately, applying these principles is central to building a more resilient organization. This aligns with the core tenets of best practices for risk management, creating an agile and durable operational framework.

Understanding the Weather Data Ecosystem

To leverage real time weather data effectively, decision-makers must understand its sources and characteristics. The journey from a raw atmospheric reading to an actionable business insight is complex, but a foundational knowledge is key to assessing data quality and selecting the right technology partners. The objective is to transform chaotic environmental signals into a structured, reliable tool for underwriting and risk management.

Consider the global financial markets. Raw data, like stock ticks, arrives from countless sources every second. This information is collected, standardized, and distributed through specialized feeds. A risk professional's goal is not to monitor every tick, but to connect to a clean, low-latency feed that delivers the specific insights required to make profitable decisions.

From Raw Observation to Actionable Insight

The modern weather data network is a sophisticated, global operation. Tens of thousands of weather stations, thousands of buoys, and dozens of satellites continuously generate petabytes of data annually.

For instance, the European Centre for Medium-Range Weather Forecasts (ECMWF) aggregates global data to create its highly regarded ERA5 dataset, which is updated with only a six-day lag. You can discover more about how global temperature data is compiled on berkeleyearth.org.

This constant stream creates a firehose of raw information that requires processing to be useful. Specialized data providers ingest these billions of data points and transform them into clean, structured API feeds optimized for business applications, ensuring the information is not just fast but also reliable and relevant.

---

Sources of Real Time Weather Data

The raw data powering any high-quality weather feed originates from several primary sources, each with a distinct function. Understanding these sources clarifies the types of insights a data provider can deliver.

| Data Source | Key Metric Examples | Typical Latency | Primary Insurance Use Case |

|---|---|---|---|

| Ground Stations | Temperature, humidity, wind speed, barometric pressure | 1-15 minutes | Hyperlocal underwriting, property-specific risk assessment, claims validation. |

| Weather Radar | Precipitation type (rain, hail), intensity, storm cell movement | 2-10 minutes | Severe convective storm warnings, hail alerts, flood risk monitoring. |

| Satellites | Cloud cover, surface temperature, atmospheric moisture | 5-30 minutes | Large-scale pattern analysis, hurricane tracking, wildfire smoke monitoring. |

| Buoys & Ships | Wave height, sea surface temperature, wind over water | 15-60 minutes | Marine underwriting, supply chain risk management, coastal property risk. |

Each source provides a piece of the puzzle. The true power emerges when a provider fuses these disparate streams into a single, coherent picture of risk.

---

Key Characteristics of Weather Data Feeds

When evaluating data providers, three critical metrics determine the data’s business value. Mastering these is fundamental to leveraging real-time data analytics for insurance effectively.

Just as an investor requires trusted market data, an insurer needs a reliable weather feed. Inaccurate or delayed information leads to mispriced risk, missed mitigation opportunities, and adverse claims outcomes.

Let’s break down the metrics that matter:

- Latency: The delay between a weather event occurring and the data appearing in your system. For proactive alerts—such as warning a client of an impending hailstorm—low latency is non-negotiable.

- Resolution: The level of detail, both geographically (street-level vs. county-level) and temporally (minute-by-minute vs. hourly). High resolution is crucial for property-specific underwriting, enabling risk assessment for a single building rather than an entire ZIP code.

- Reliability: The feed's consistency and accuracy. A reliable provider ensures their data is clean, error-free, and available—especially during major weather events when it is most needed.

A solid grasp of this ecosystem empowers you to ask the right questions and select a data partner that delivers not just information, but true operational intelligence.

Transforming Underwriting with Granular Insights

A group of insurance professionals analyzing weather data on a large screen

For decades, underwriting has balanced historical claims data against generalized risk models. In an era of increasing climate volatility, this traditional approach is failing. Static, ZIP code-level assessments cannot capture the property-specific exposures that define true risk.

This is where real time weather data fundamentally alters the underwriting process.

By shifting from broad regional averages to live, hyperlocal conditions, underwriters can price risk with surgical precision. This is not an incremental improvement; it is a paradigm shift in risk evaluation.

Instead of asking, "What is the hail risk in this county?" an underwriter can now ask, "What is the specific hail size and frequency risk for *this exact commercial building*, given its roof specifications and location within a known storm corridor?" This granularity leads to more accurate pricing, reduces adverse selection, and strengthens the entire underwriting portfolio.

From Static Models to Dynamic Risk Assessment

The primary flaw in traditional risk models is their reliance on outdated information. A property’s risk profile is not a fixed variable; it changes with every approaching storm and shift in local environmental conditions. High-resolution weather data transforms risk assessment into a dynamic, real-time process.

Consider a commercial policy for a warehouse complex. A static model may flag it as being in a moderate flood zone based on historical maps that are years or even decades old.

A dynamic approach, powered by real time weather data, provides a much clearer picture. It can analyze current soil saturation levels, monitor upstream river gauges, and model the potential impact of an incoming storm system with unprecedented accuracy.

This allows underwriters to make decisions based on what is happening *now* and what is likely to happen *next*, rather than relying on a historical view.

Practical Applications in Commercial Underwriting

The business impact of this precision is immediate. By integrating hyperlocal data, underwriters can confidently price policies that were once too ambiguous to assess, opening new market opportunities while mitigating potential losses.

Here are specific examples of its application:

- Wildfire Risk Assessment: Instead of using only a static risk map, an underwriter can analyze real-time wind direction and speed data to model the path of embers. This helps pinpoint the threat to a commercial property miles from the fire, allowing for sharper pricing and targeted mitigation advice.

- Hail Damage Vulnerability: A policy for a large retail store with an expansive, flat roof can be priced more accurately by analyzing real-time and forecast hail data. Underwriters can assess risk based on the probable size of hailstones and storm frequency in that *specific* location, not just the broader region.

- Flash Flood Exposure: For a business in a low-lying urban area, underwriters can use live precipitation intensity data layered with topographical information. This enables them to model the immediate risk of flash flooding from a severe thunderstorm—a peril that broad-stroke flood maps often miss.

These granular insights allow underwriters to move beyond a one-size-fits-all model. By understanding the unique environmental threats to each asset, they can write more equitable and accurate policies. This sophisticated approach is a core component of modern business intelligence for insurance, turning raw data into profitable decisions.

Ultimately, this precision unlocks the ability to underwrite risks that might have been previously deemed uninsurable, creating new revenue streams while protecting the book of business.

Accelerating Claims and Enhancing Customer Loyalty

An insurance claims adjuster works on a laptop in front of a storm-damaged building

For an insurance carrier, the claims experience is the ultimate moment of truth. It is when a policy transitions from a document to a critical financial lifeline for a client in crisis. Speed, accuracy, and empathy are paramount, and real-time weather data provides the foundation for all three.

Traditionally, processing claims after a major weather event is a slow, manual, and expensive process. Adjusters must be deployed, damage assessed on-site, and the cause of loss verified—all while the policyholder waits. This not only increases loss adjustment expenses (LAE) but also erodes customer trust.

Access to event-specific data changes the entire process. By integrating live weather feeds, claims teams can instantly see the exact conditions at a specific property at the precise time of loss. This objective, third-party data serves as a powerful validation tool, confirming whether a claim aligns with the recorded event.

Automating Validation and Reducing Expenses

The ability to instantly cross-reference a claim with hyperlocal weather data delivers a massive operational advantage. This data-driven validation dramatically reduces the need for manual investigations and on-site visits for many claims, translating directly to cost savings.

Consider these scenarios:

- Hail Damage: Instead of dispatching an adjuster to measure roof dents, the system can retrieve real-time radar data confirming that hail of 1.5 inches in diameter passed directly over the insured property at the reported time, potentially triggering an immediate, automated approval.

- Wind Damage: A claim for roof damage can be validated against ground-level wind speed measurements. If data shows gusts exceeded 75 mph at the property's coordinates, the claim's legitimacy is instantly supported, expediting payment.

- Flood Claims: Real-time rainfall and sensor data can confirm precipitation intensity and duration, helping to differentiate a covered flash flood from an uncovered issue like a sewer backup.

By automating this initial validation step, insurers can fast-track legitimate claims, reduce fraudulent payouts, and slash their loss adjustment expenses. This allows human adjusters to focus their expertise on the complex cases where they are needed most.

The impact of such systems extends beyond insurance. The United Nations estimates that robust early warning systems, powered by real-time data, can reduce disaster-related mortality by up to 80%.

The Rise of Parametric Insurance

The most direct application of real-time weather data in claims is the growth of parametric insurance. Unlike traditional insurance that pays based on the *actual loss* incurred, a parametric policy pays a pre-agreed amount when a specific, measurable event occurs.

This model is remarkably simple and efficient. The trigger for a payout is not a lengthy damage assessment—it is the weather data itself.

- A policy might stipulate that if a Category 3 hurricane (defined by sustained wind speeds) makes landfall within a specified radius of a commercial property, a $250,000 payout is automatically released.

- For an agricultural business, a drought policy could trigger a payment if rainfall at a designated weather station falls below a certain threshold for 90 consecutive days.

There is no prolonged claims process or dispute over the extent of the damage. The payout is triggered automatically by the verified weather event, often delivering funds to the policyholder in days, not months. This speed is a critical advantage for businesses needing immediate capital for recovery, a key element discussed in our guide to disaster preparedness for businesses.

This data-first model not only creates massive operational efficiencies but also builds profound customer loyalty. When a business receives essential funds immediately following a disaster, its insurer becomes a true partner in recovery.

Driving Proactive Portfolio-Level Risk Mitigation

<iframe width="100%" style="aspect-ratio: 16 / 9;" src="https://www.youtube.com/embed/r3_JTORLn6Y" frameborder="0" allow="autoplay; encrypted-media" allowfullscreen></iframe>

Analyzing risk on a policy-by-policy basis is fundamental, but a strategic advantage comes from viewing the entire portfolio through the lens of real time weather data. This approach transforms risk management from a defensive posture to a proactive operation that protects both capital and clients.

Instead of waiting for loss reports after a major storm, portfolio managers can now anticipate impacts and act decisively. This shifts the focus from managing individual losses to building holistic portfolio resilience—a move from post-event damage control to pre-event strategic action.

By monitoring an incoming weather system, an insurer can send targeted alerts to commercial clients in the storm's path, providing the crucial time needed to secure assets and mitigate potential damages before the event arrives.

Identifying Hidden Risk Concentrations

A significant blind spot in traditional portfolio management is hidden risk concentration. A portfolio may appear diversified across a state, but this can create a false sense of security.

A high percentage of those properties might lie within a specific severe storm corridor. Perils like understanding surface water flooding can cluster in ways that geography alone does not reveal. These concentrated vulnerabilities remain invisible until a major event exposes them, resulting in staggering, unexpected losses.

By layering live weather data over a portfolio map, you can instantly identify which policies are in the direct path of an approaching hailstorm or potential flash flood. This dynamic view of risk is something static models cannot provide.

This clarity enables risk managers to make smarter decisions on capital allocation and reinsurance. It provides the hard evidence needed to adjust treaties, secure appropriate coverage, and ensure the portfolio is genuinely protected against large-scale threats.

From Risk Manager to Strategic Advisor

When you possess real-time weather intelligence, you fundamentally change your relationship with clients. Brokers and carriers evolve from policy providers to indispensable risk advisors, creating immense value and fostering fierce loyalty.

- Targeted Loss Prevention Alerts: Automatically notify clients in an area about to be impacted by damaging hail, advising them to move vehicle fleets under cover.

- Pre-Event Resource Deployment: Help clients connect with vetted contractors to board up windows or clear drainage systems before a hurricane makes landfall.

- Post-Event Triage: Immediately after a storm, identify the hardest-hit clients and deploy claims teams to them first, providing support when it is needed most.

This advisory role is a powerful differentiator in a competitive market. This analysis is also becoming critical in a changing climate. While real time weather data is used for short-term events, it also populates the long-term datasets that track climate trends. Global monitors show the ten hottest years on record have all occurred since 2014, with January 2025 being the warmest January ever recorded.

These trends underscore the importance of data-driven mitigation. For a closer look at the technologies enabling this, see our guide on available climate risk assessment tools. By embedding these capabilities into your workflow, you create a more resilient portfolio and solidify your position as an industry leader.

Integrating Weather Data into Your Operations

Two professionals discussing a data integration roadmap on a whiteboard

Understanding the value of real time weather data is one thing; integrating it into daily workflows is another. The goal is to move beyond concepts and build a practical system that delivers measurable business results. This requires a methodical approach that starts with a pilot, proves its value, and then scales intelligently.

The first step is selecting the right technology partner. When evaluating third-party data providers, you are acquiring more than just data. It is crucial to assess the ease of API integration, system reliability during major events, and their ability to deliver the specific data points relevant to your portfolio.

Building Your Implementation Framework

Successful integration starts with a focused pilot project designed to solve one specific business problem. This strategy minimizes initial investment, provides your team with hands-on experience, and helps build a compelling business case for a wider rollout.

A well-designed pilot serves as your proof of concept. It must have a clear, measurable objective, such as reducing claims validation time for hail events or improving risk selection for a single line of business.

This focused strategy is designed to achieve a quick, tangible win that secures the executive buy-in needed for full-scale integration.

Starting Small and Proving Value

Select a pilot project with a high probability of success. A strong starting point is often automating claims verification for severe convective storms. The goal is simple: use real-time hail size or wind speed data to fast-track legitimate claims while flagging questionable ones for review. The impact on operational efficiency is immediate and quantifiable.

To build an airtight business case, define success metrics before you begin. These metrics must be directly tied to business performance.

Key Metrics to Measure ROI:

- Improved Loss Ratios: Track the performance of a pilot group using data-driven underwriting against a control group. The difference in incurred losses is your proof of value.

- Faster Claims Cycles: Measure the reduction in days from First Notice of Loss (FNOL) to payment for claims validated with weather data.

- Reduced Loss Adjustment Expenses (LAE): Quantify savings from fewer on-site inspections and less manual verification work.

- Increased Underwriting Capacity: Demonstrate how automated data feeds allow underwriters to assess more policies with greater accuracy in the same amount of time.

Focusing on these concrete numbers shifts the conversation from technology to business strategy. A successful pilot provides the hard data and momentum required to integrate real time weather data across your entire operation, creating a sustainable competitive advantage.

Common Questions About Weather Data Integration

When considering the integration of real-time weather data, several practical questions consistently arise. Addressing these is essential before embedding this intelligence into your underwriting, claims, and risk management workflows.

Clarifying these details builds the confidence needed to move from evaluation to implementation.

How Accurate and Reliable Is This Data?

Top-tier commercial weather data is exceptionally accurate. It is not derived from a single source but is a fusion of inputs—ground stations, Doppler radar, satellite imagery—all cleansed and standardized by proprietary algorithms.

This process is engineered to eliminate errors and ensure consistency, which is critical when a major storm is approaching and system uptime is non-negotiable.

For insurance applications, this means the data is precise enough to validate conditions at a specific property. You can confirm the exact wind speed or hail size at an individual address during an event.

The primary value is third-party objectivity. This data provides a verifiable, scientific record of what occurred, removing subjectivity from claims validation and risk assessment.

What Is the Typical Cost and ROI?

The cost depends on your specific needs: the provider, data granularity, and scope of implementation. Many modern platforms operate on flexible models, such as pay-per-use or subscription tiers.

This approach allows you to avoid significant upfront capital expenditures. You can begin with a focused pilot project and scale as the value is proven.

Measuring the return on investment is straightforward. Focus on key operational metrics:

- Improved Loss Ratios: Achieved by writing more accurately priced policies and proactively managing risk.

- Reduced LAE: Gained by automating claims validation and decreasing the need for on-site inspections.

- Increased Underwriter Productivity: Realized by providing underwriters with instant access to critical risk data.

A successful pilot can demonstrate a positive ROI quickly, providing a data-driven business case for expanding the rollout across the organization.

---

Ready to turn climate events into high-intent business opportunities? With Insurtech.bpcorp.eu, you gain access to validated corporate leads affected by severe weather, delivered within 24 hours. Stop reacting and start proactively engaging with clients at their moment of greatest need. Discover your next opportunity at https://insurtech.bpcorp.eu.