For decision-makers in commercial insurance, geospatial intelligence (GEOINT) transforms location data into a distinct competitive advantage. It moves beyond static maps by layering dynamic, asset-level data—such as high-resolution satellite imagery, real-time weather alerts, and property characteristics—onto a single geographic point.

The result is a dynamic, actionable risk profile for every asset in your portfolio.

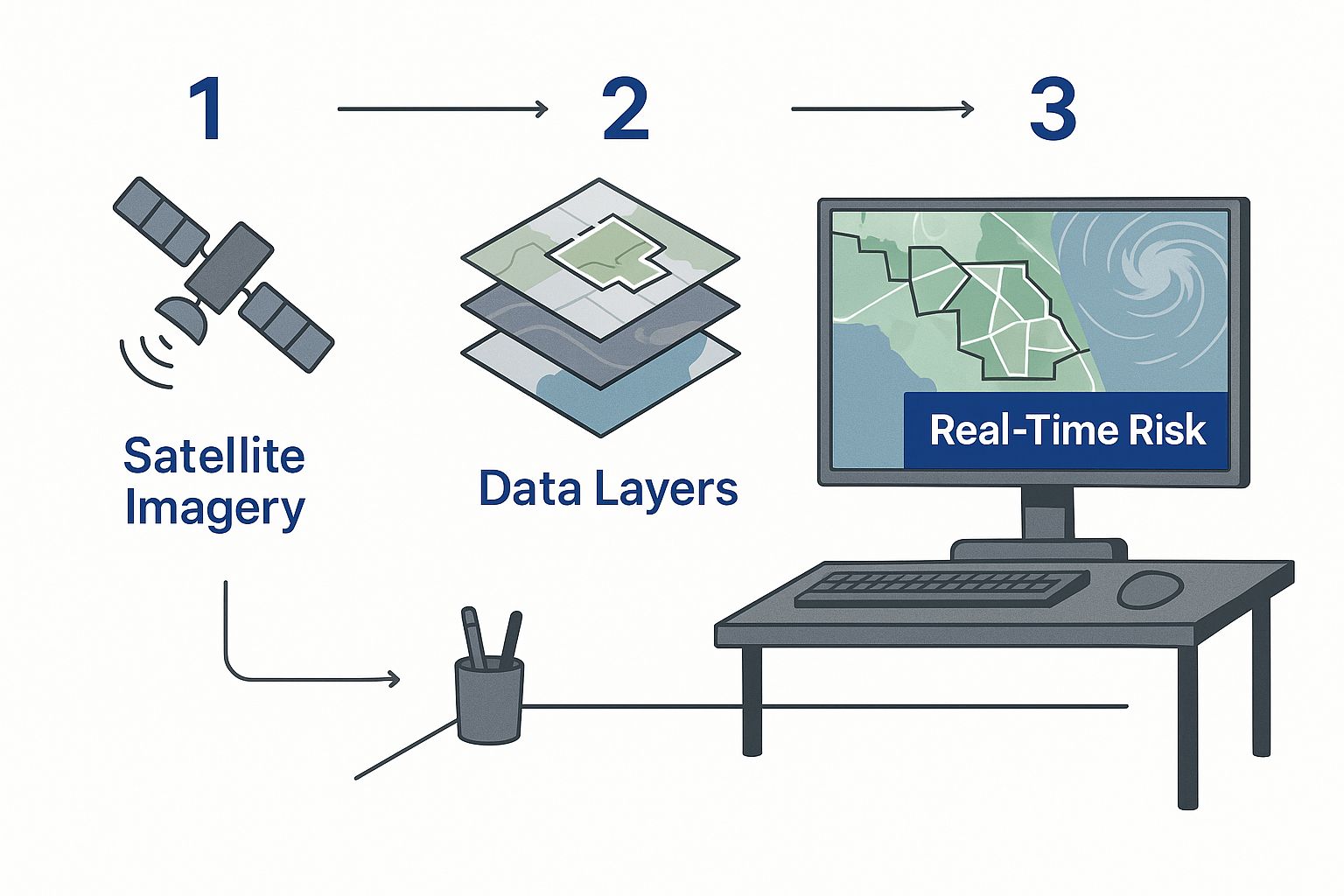

From Maps to Strategic Decisions

In the commercial insurance and climate risk sectors, "geospatial intelligence" is no longer a mapping tool; it is a core strategic asset. It is the analytical engine that processes raw, location-based data and converts it into clear, actionable insights for underwriting, risk management, and claims processing.

This discipline functions by integrating imagery intelligence (IMINT) with geospatial information to create a comprehensive, near-real-time understanding of on-the-ground conditions.

The infographic below illustrates this process, showing how modern platforms aggregate diverse data sources—from satellite feeds to property-specific attributes—into a unified view for immediate risk assessment.

Infographic about what is geospatial intelligence

The primary value is the convergence of this information. It enables underwriters and risk managers to shift from reactive calculations to proactive, data-driven risk strategies.

The Business Value of Geographic Context

At its core, GEOINT answers critical business questions by adding precise geographic context. Instead of knowing a hurricane is approaching a coastal state, you can pinpoint the specific insured properties in its direct path, analyze their structural vulnerabilities remotely, and accurately forecast potential claims volume before landfall.

This capability is driving significant investment. The global geospatial analytics market was valued at USD 83.93 billion in 2024 and is projected to reach USD 230.88 billion by 2033, reflecting a compound annual growth rate of nearly 12%.

Geospatial intelligence provides the definitive "where" and "why" behind risk. For an underwriter, this means assessing a property not just by its ZIP code, but by its precise elevation, its proximity to wildfire fuel, and historical storm surge data.

To understand its value, it is essential to break GEOINT into its core components.

Core Components of Geospatial Intelligence

This table outlines the key elements of GEOINT and their direct application in the insurance industry.

| Component | Description | Example in Insurance |

|---|---|---|

| Imagery Intelligence (IMINT) | Analysis of satellite, aerial, and drone imagery to identify and assess physical objects and activities. | Using post-hurricane satellite imagery to assess roof damage across an entire commercial district, enabling rapid claims triage. |

| Human Geography | Data related to human presence, including demographics, infrastructure, and economic activity. | Mapping population density and commercial building locations to model potential business interruption losses from a tornado. |

| Signals Intelligence (SIGINT) | Information derived from electronic signals, often used for real-time event tracking and communication patterns. | Tracking cellular network activity to understand evacuation patterns and population movement during an active wildfire event. |

| Measurement & Signature Intelligence (MASINT) | Technically-derived intelligence that detects, identifies, or describes the distinct characteristics of targets. | Using spectral analysis from satellite imagery to differentiate between healthy crops and those affected by drought for agricultural insurance claims. |

Each data stream contributes to a holistic analytical process, creating a more accurate and comprehensive picture of risk than any single source can provide.

Beyond Location Intelligence

While related, GEOINT is more than standard location analytics. It is an intelligence product created through a structured process: collecting, analyzing, and visualizing data to support a specific business decision.

This distinction is critical for insurers navigating escalating climate uncertainty. A successful strategy requires more than dots on a map; it demands predictive insights that inform pricing, portfolio management, and rapid claims response.

To see the tools that enable this, review our guide on the best location intelligence software. This foundation enables smarter, more profitable decisions in an increasingly volatile market.

How Raw Data Becomes Actionable Insight

A simplified diagram showing data from satellites and drones being processed by AI and turned into a visual risk map on a computer screen.

Geospatial intelligence is not abstract technology; it is a methodical process that transforms vast volumes of raw location data into decisive business insights.

This journey from data to decision is built on three pillars. Each stage builds on the last, delivering tangible value directly to underwriters, claims adjusters, and risk managers.

It begins with acquiring the right information.

Stage 1: Data Acquisition

The foundation of any credible intelligence product is the quality of its source data. This first step involves collecting extensive geospatial information from diverse, advanced sensors and platforms to build the most complete, up-to-date picture of a specific location.

Key data sources include:

- Satellite Imagery: High-resolution optical and radar images from commercial satellite constellations provide a continuous stream of information on ground-level changes.

- Aerial and Drone Surveys: For granular analysis, drones and aircraft capture detailed, property-level imagery essential for assessing specific risk factors like roof conditions or vegetation encroachment.

- On-the-Ground Sensors: Data from IoT devices, weather stations, and river gauges deliver real-time metrics on critical conditions such as rainfall, wind speed, and water levels.

This collected data—a mix of pixels, numbers, and signals—holds immense potential but is unusable in its raw state. The next stage forges it into something meaningful.

Stage 2: Analysis and Processing

This is where artificial intelligence and machine learning algorithms perform the heavy lifting. Human analysts cannot manually process petabytes of satellite imagery or sensor data at the speed required for modern business decisions.

Instead, sophisticated models analyze the information to detect patterns, classify objects, and model potential outcomes.

For example, an AI model trained on millions of images can automatically identify properties with significant tree overhang in a high-risk wildfire zone. Another algorithm can analyze historical rainfall data and real-time sensor readings to predict flash flood depths for a specific commercial district. To understand this better, read our article on real-time data analytics and its application in insurance.

The analysis phase separates GEOINT from a simple map. It transforms a static picture of a property into a dynamic risk forecast, answering the critical question: "What is likely to happen here?"

This analytical output is powerful but must be presented in a format that enables quick, confident decisions.

Stage 3: Visualization and Dissemination

This final stage is the most critical for risk management professionals. All complex analysis must be translated into an intuitive and immediately actionable format.

A busy underwriter does not have time to interpret raw analytical outputs; they need a clear signal, not more noise.

This is where tools like interactive dashboards, heat maps, and automated alert systems become essential. For example, deep analysis identifying a property's flood risk is distilled into a simple risk score from 1 to 10. The output of a wildfire model becomes a clear visual overlay showing the projected burn path relative to an insured portfolio.

This final step ensures the intelligence is not just accurate but immediately usable, empowering teams to act decisively.

Applying Geospatial Intelligence to Climate Risk

<iframe width="100%" style="aspect-ratio: 16 / 9;" src="https://www.youtube.com/embed/jpEGrZfdg98" frameborder="0" allow="autoplay; encrypted-media" allowfullscreen></iframe>

Having outlined the GEOINT process, let's focus on its practical application. Forward-thinking insurers are not just experimenting with this technology; they are embedding geospatial intelligence into core operations to gain a durable competitive edge in managing climate risk.

GEOINT delivers tangible results by solving specific, high-stakes business problems. It moves decision-making from reactive and assumption-based to proactive and data-driven. From pinpointing a single building’s hail exposure to accelerating post-hurricane claims, it offers measurable value. For a closer look at the platforms making this possible, see our deep dive into the leading climate risk assessment tools.

Precision Underwriting and Risk Selection

For underwriters, the primary benefit is the shift away from broad, regional risk modeling. In today's volatile climate, relying on ZIP-code-level data for perils like wildfires or hurricanes is an outdated and inefficient approach. Geospatial intelligence delivers surgical precision at the individual property level.

Consider an underwriter evaluating a commercial property in a wildfire-prone region. Previously, they might only know it is in a high-risk county. Today, GEOINT provides a much richer view:

- The property’s exact distance to the nearest dense vegetation, or fuel load.

- Historical burn scars showing the proximity of previous fires.

- The slope and aspect of the land, which are critical factors in fire behavior.

This granularity enables underwriting and pricing that accurately reflect on-the-ground reality, preventing insurers from writing underpriced policies that erode profitability.

Accelerating Claims and Detecting Fraud

The claims department is where GEOINT demonstrates its operational strength, particularly in the aftermath of a major catastrophe. Following a hurricane, claims teams are inundated with First Notices of Loss (FNOL). Deploying adjusters to every property is slow, expensive, and often hazardous.

Using post-event satellite and aerial imagery, insurers can now triage damage across entire portfolios in hours, not weeks. AI models scan thousands of images, automatically flagging the severity of roof damage, flooding, or structural collapse.

This is not just about speed; it is about smarter resource allocation. Geospatial intelligence helps claims managers direct field teams to the hardest-hit properties first, improving customer satisfaction and significantly reducing the claims lifecycle.

The same imagery is also a powerful tool against fraud. If a policyholder claims a total roof loss but high-resolution imagery shows only minor damage, the discrepancy is flagged instantly for review.

Proactive Portfolio Management

For portfolio and risk managers, GEOINT offers a macro-level view of risk concentration that was previously unattainable. On a spreadsheet, a portfolio might appear balanced. A geospatial analysis, however, can reveal hidden risk concentrations invisible in standard reports.

For instance, a manager might discover that a seemingly diverse book of business has a dangerous number of properties clustered within a half-mile of a coastline projected to see severe storm surge. This insight allows them to act *before* an event by tightening underwriting guidelines in that specific area or purchasing targeted reinsurance.

The strategic importance of this technology is significant. The global geospatial analytics market is projected to reach USD 174 billion by 2030. You can explore this growth further at Mordor Intelligence.

Geospatial Intelligence Use Cases Across Insurance

The following table demonstrates how different insurance functions apply GEOINT to solve specific business problems related to climate risk.

| Insurance Function | Business Challenge | GEOINT Application | Key Benefit |

|---|---|---|---|

| Underwriting | Inaccurate risk pricing based on outdated, broad-area models. | Analyze property-specific peril data (wildfire fuel, flood elevation, hail history). | Price policies with precision, avoiding unprofitable risks. |

| Claims | Slow, expensive post-catastrophe response and high fraud potential. | Use post-event imagery (satellite, drone) to triage damage and verify claims. | Faster claims settlement, lower operational costs, and reduced fraud. |

| Portfolio Management | Unseen risk concentrations that threaten portfolio stability. | Map entire portfolio against multiple climate peril layers to identify hidden hotspots. | Proactive risk mitigation and more strategic reinsurance purchasing. |

| Product Development | Inability to create innovative, parametric insurance products. | Leverage real-time and historical data feeds (e.g., wind speed, rainfall) as triggers. | Launch new products based on objective, verifiable data triggers. |

Each of these applications demonstrates a shift from a generalized to a highly specific understanding of risk, empowering insurers to make smarter, faster, and more profitable decisions in the face of increasing climate uncertainty.

The Technology Driving Modern GEOINT

A satellite in orbit above Earth, with beams of light connecting it to data centers on the ground, representing data transmission.

Today’s geospatial intelligence is powered by a convergence of advanced technologies that transform raw location data into a strategic asset. For insurance leaders evaluating new technology partners, understanding the underlying components is crucial.

It begins with advanced remote sensing. A growing fleet of commercial satellites provides a constant, near-real-time stream of high-resolution Earth imagery. This is not a static picture but a live feed that captures change as it happens—from new construction to the initial smoke of a wildfire.

This stream of visual data is just the starting point. The true value is unlocked during processing.

The GIS and AI Powerhouse

At the core is the Geographic Information System (GIS). GIS acts as the digital command center where all spatial data is layered, organized, and prepared for analysis. It is the platform that allows an underwriter to view a property not just as an address but as a point with specific attributes like elevation, soil type, and proximity to a floodplain.

However, GIS alone cannot manage the volume and velocity of modern data. This is where Artificial Intelligence (AI) and Machine Learning (ML) are transformative. Modern geospatial intelligence is supercharged by AI. For a broader view, see these AI Technology and Innovations Industry Insights and Trends.

AI algorithms automate the labor-intensive task of feature extraction. For instance, an ML model can:

- Scan thousands of aerial images to automatically flag properties with undeclared swimming pools, a significant liability risk.

- Analyze spectral imagery to detect early signs of roof degradation or moisture stress, indicating a higher risk of future claims.

- Monitor vegetation growth to identify properties with dangerously high wildfire exposure.

AI doesn't just identify existing conditions. It powers the predictive models essential for proactive risk management. It is the intelligence that forecasts a hurricane’s path with greater accuracy or models floodwater depth during a flash flood.

From Detection to Prediction

The combination of constant remote sensing, powerful GIS organization, and intelligent AI analysis makes modern GEOINT effective. It shifts the focus from passively observing past events to actively predicting future outcomes.

For insurers, this enables underwriting with confidence based on current, property-specific conditions. The accuracy of these models is paramount. For a closer look at model validation, you can explore our detailed breakdown of the Sentinel accuracy methodology.

Ultimately, this technology stack provides the clarity required to navigate an increasingly complex and volatile risk environment.

Integrating GEOINT into Your Underwriting Workflow

Integrating geospatial intelligence into your underwriting workflow does not require a complete operational overhaul. A successful integration enhances existing processes with spatially-aware, data-driven insights. The most effective approach is to begin with a single, focused pilot project.

Start by targeting one high-value problem. For instance, you could focus on improving wildfire exposure analysis for a portfolio in a single high-risk state. Alternatively, you could automate hail risk assessments for commercial properties in a specific territory.

This targeted approach demonstrates ROI quickly, builds internal momentum, and proves the technology's value without disrupting your entire operation. A successful pilot makes the business case for broader adoption.

Starting with a Focused Pilot

To launch a successful pilot program, follow a clear, strategic path:

- Define a Specific Goal: Start with a measurable objective, such as, "Reduce our wildfire risk misclassification rate by 15% in California," or "Decrease initial hail damage assessment time from 48 hours to 4 hours."

- Select the Right Data: Partner with a provider that can deliver the exact geospatial data needed to achieve your goal, whether it's high-resolution aerial imagery, historical storm data, or detailed vegetation density maps.

- Integrate and Test: Ensure the new data feeds directly into a test environment of your current underwriting platform. The objective is to enhance the tools your team already uses, not replace them.

- Measure and Report: Track performance against your stated goal. A successful pilot will yield hard numbers on improved accuracy, speed, or loss avoidance that you can present to key stakeholders.

This methodical approach minimizes risk while maximizing the potential for securing buy-in for a wider rollout. The importance of this field is clear; geospatial intelligence is projected to be central to a USD 1.44 trillion global market by 2030. More details on this growth are available in a report by Geospatial World.

The Build Versus Buy Decision

As you plan your integration, you will face the "build vs. buy" decision. Building a GEOINT capability from scratch offers complete customization but requires a significant investment in specialized talent, data acquisition, and technology infrastructure.

For most insurers, partnering with a specialized vendor is the more practical and efficient path. A dedicated GEOINT provider offers several advantages:

- Access to pre-built and validated risk models.

- Continuously updated and diverse datasets from multiple sources.

- Deep expertise in integrating insights seamlessly into existing systems via APIs.

A partnership allows you to leverage advanced capabilities immediately, accelerating your time-to-value without the significant overhead of an in-house build. This approach connects your core operations with a steady stream of actionable intelligence.

This operational upgrade is a key component of a larger strategy. To understand the broader context, review the concepts in our guide on business intelligence for insurance.

For a practical example of how GEOINT improves efficiency, see how geo-location data strengthens insurance claims, which provides the verified evidence underwriters need. The ultimate goal is to make data-backed decisions a routine part of your daily workflow.

Your Top Questions, Answered

Integrating new technology into established workflows raises practical questions regarding cost, accuracy, and complexity. Here are direct answers to the most common questions from insurance leaders.

Isn't Geospatial Intelligence Just a Fancy Name for GIS?

No, though they are closely related. A Geographic Information System (GIS) is the underlying technology—the software and hardware used to store, manage, and analyze location-based data. It is the platform that performs the heavy lifting.

Geospatial Intelligence (GEOINT) is the finished analytical product derived from that platform. It is the clear, actionable answer to a specific business question, formatted for a decision-maker.

An analogy: GIS is the professional kitchen with all the necessary appliances and ingredients. GEOINT is the fully prepared meal delivered to your desk, ready for consumption.

How Is This Different from Our Catastrophe Models?

They serve two different yet complementary purposes. Traditional catastrophe (CAT) models are essential for long-term strategic planning and reinsurance. They provide a broad, probabilistic view of risk to answer questions like, "What is our probable maximum loss for a 1-in-100-year flood in this region?"

GEOINT operates on a more immediate and granular level. It provides a deterministic, near-real-time view of risk for a specific property. It is designed to answer tactical questions like, "Which of my policyholders are in the direct path of this wildfire *right now*?"

In short, CAT modeling shapes long-term strategy, while GEOINT drives immediate operational decisions.

What's the Smartest Way to Get Started?

Start with a single, high-value problem. The most common mistake is attempting a complete overhaul at once. Instead, launch a focused pilot project designed to deliver a clear, measurable business outcome.

Proven starting points for a pilot include:

- Refine Flood Risk Scoring: Select a specific coastal portfolio and use GEOINT to improve flood risk assessments, moving beyond generic FEMA zones to property-level elevation data.

- Automate Hail Risk Assessment: Choose a key state and automate your property-level hail exposure analysis for a book of commercial buildings.

- Improve Wildfire Triage: Focus on a high-risk territory and use real-time data to prioritize underwriting submissions or fast-track claims inspections after an event.

A successful pilot project generates tangible ROI and builds internal expertise. More importantly, it secures the stakeholder buy-in required to implement a more ambitious program. Partnering with a specialized vendor can de-risk this initial step and accelerate your first win.

---

Ready to turn climate risk into a measurable business advantage? Insurtech.bpcorp.eu delivers real-time, actionable intelligence on businesses impacted by climate events, providing you with high-intent opportunities exactly when they need you most. Discover how Sentinel Shield can fuel your growth at https://insurtech.bpcorp.eu.