Behavioral targeting moves beyond static applications to provide a real-time view of a potential client’s risks and intentions. It is the practice of understanding what a commercial client needs by analyzing their digital actions. This data-driven approach enables precise, relevant outreach based on demonstrated intent rather than assumptions.

Uncovering Commercial Risk Through Digital Behavior

An experienced broker assesses a client not just on their stated needs but on their tone, inquiries, and areas of concern. This "body language" often reveals a more accurate risk profile than a standard questionnaire. Behavioral targeting applies this same principle to the digital realm.

It analyzes a prospect’s online actions—their “digital body language”—to build a sophisticated risk profile. By tracking browsing history, content engagement, and search queries, insurers can anticipate needs and offer relevant solutions at the optimal time.

For example, a risk manager consistently researching articles on supply chain disruptions signals a specific operational vulnerability. This insight is significantly more powerful than a generic lead form submission. Translating these signals into a coherent strategy is a core function of modern business intelligence for insurance.

This is not a niche tactic; it is a market expectation. A Deloitte study found that 80% of consumers are more likely to do business with companies offering personalized experiences. This demonstrates the powerful demand for the tailored engagement that behavioral targeting delivers.

Image

The objective is to stop guessing what clients need and start responding to what their actions demonstrate. It is about engaging proactively based on observed interest, which provides a stronger foundation for any business relationship.

Core Components of Behavioral Targeting

The process can be broken down into three fundamental pillars. These components work in sequence to convert raw digital behavior into actionable business intelligence.

| Component | Description | Example in Commercial Insurance |

|---|---|---|

| Data Collection | Gathering anonymized information about a user's online activities across digital touchpoints. | A potential client visits an insurer's website and downloads a whitepaper on commercial flood risk. |

| Segmentation | Grouping users into distinct audiences based on shared behaviors, interests, or inferred intent. | Creating a segment of "Logistics Risk Managers" who have viewed content related to cargo theft. |

| Personalization | Delivering tailored messages, content, or policy information to a specific audience segment. | Serving a digital ad for a specialized cargo insurance policy to the "Logistics Risk Managers" segment. |

By mastering data collection, intelligent segmentation, and personalized outreach, insurers can transition from broad-based marketing to precision-guided engagement that resonates with each high-value commercial prospect.

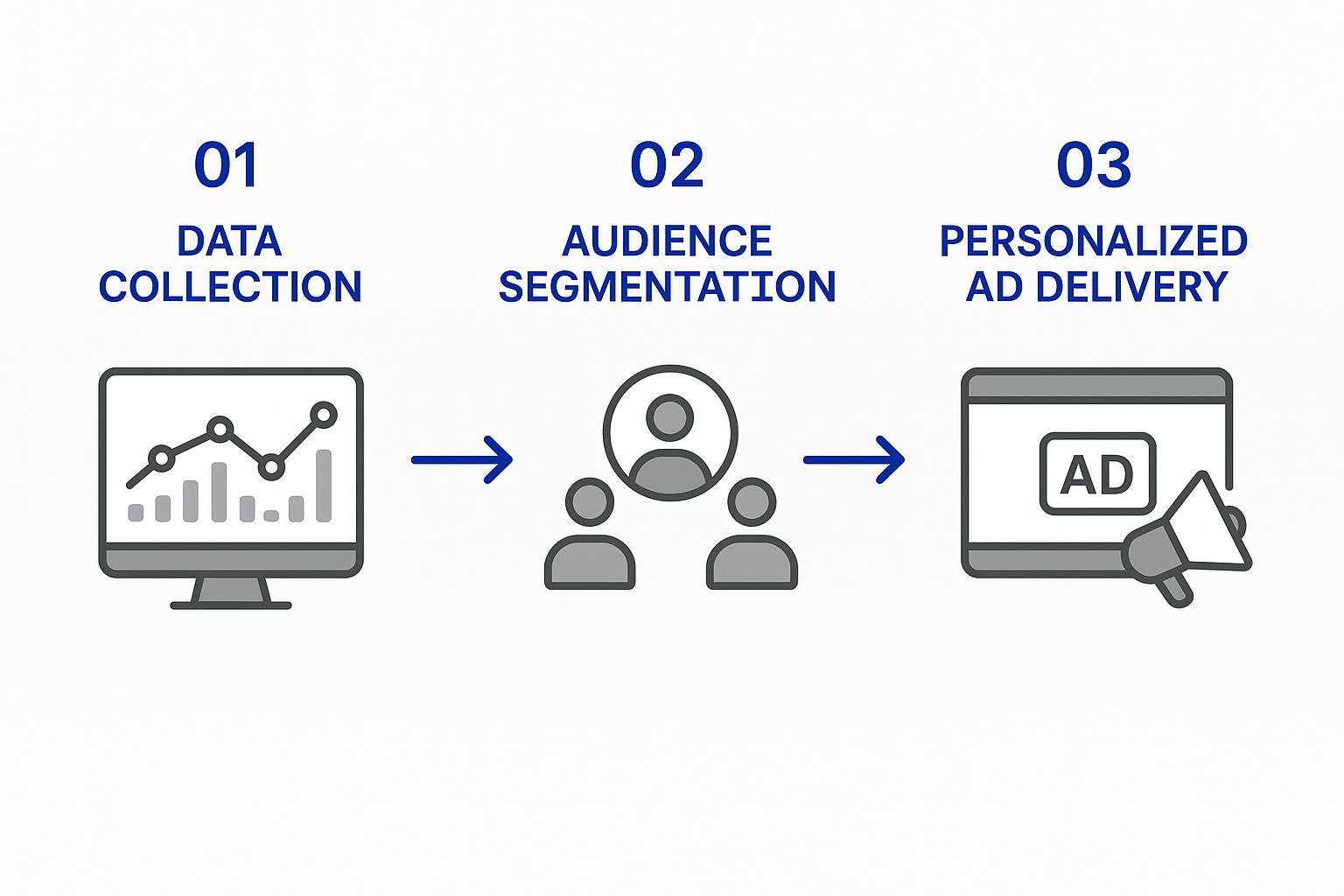

How the Behavioral Targeting Process Works

Behavioral targeting transforms anonymous digital footprints into direct, personalized business conversations. The process involves systematically gathering data, organizing audiences into meaningful groups, and delivering content that addresses specific business pains.

It begins with collecting information from proprietary digital assets. This first step is about gathering first-party data—information collected directly from a company website or client portal. This includes tracking which articles a risk manager reads, which policy pages they revisit, or which risk assessment tools they use. This proprietary data can then be enriched with anonymized third-party signals to build a comprehensive view of a potential client's current needs and purchasing intent.

This flowchart provides a high-level overview of the core stages, from initial data collection to final, targeted delivery.

Infographic about what is behavioral targeting

As illustrated, each stage builds logically on the previous one. Raw behavioral data is progressively refined into a specific, relevant marketing action designed to generate a qualified lead.

Audience Segmentation and Profiling

Once data is collected, the next critical phase is audience segmentation. Algorithms analyze behavioral cues to group users into distinct segments based on their inferred interests and immediate needs. This is the point where raw data becomes actionable business intelligence.

For example, an underwriter can create a segment for "risk managers researching supply chain vulnerabilities." This group would include individuals who have downloaded whitepapers on logistical risks or registered for webinars on global trade disruptions. By creating such precise profiles, insurers can stop broadcasting generic messages and start addressing the specific concerns of their most valuable prospects.

This level of segmentation enables direct communication about a prospect's most pressing challenges. Instead of a broad campaign on "commercial insurance," a targeted message about mitigating specific supply chain risks can be delivered to an audience known to be actively seeking solutions.

Personalized Delivery and Engagement

The final step is delivering personalized content to these defined segments. A company identified as researching climate-related operational risks might be served an advertisement for a parametric insurance policy designed for extreme weather events. This timely relevance is the direct result of effective data analysis.

Executing this at scale requires a robust marketing automation implementation to manage the delivery of the right message to the right person at the optimal moment. For insurance professionals, applying these insights is critical. For a deeper analysis, review our article on leveraging real-time data analytics. The entire process creates a responsive, efficient system for connecting with clients based on what their actions—not just their words—indicate they need.

Gaining a Competitive Edge in Risk Management

An underwriter analyzing risk data on a computer screen

For insurance professionals, behavioral targeting is a core component of strategic risk management. It provides underwriters, brokers, and risk managers with a distinct advantage in a competitive market.

By focusing on specific digital behaviors, you can optimize how you identify, engage, and retain high-value commercial clients. This strategy is not about casting a wide net; it is about concentrating resources on prospects already signaling a need for your specific risk solutions. The result is a significantly higher return on business development efforts.

Elevate Lead Quality and Underwriting Efficiency

The most immediate benefit of behavioral targeting is a substantial improvement in lead quality. It allows you to pinpoint businesses actively researching the very risks you cover. For instance, identifying a company whose executives are consuming articles on director and officer liability represents a timely, high-intent opportunity, not a cold lead.

This insight also enhances the underwriting process. Early visibility into a prospect’s specific concerns—such as engagement with content on supply chain disruptions or climate-related business risks—provides underwriters with a significant head start in their assessment. This pre-qualification saves time and contributes to more accurate initial pricing models.

Behavioral targeting allows you to enter the conversation at the precise moment a prospect identifies a problem. You are no longer just selling insurance; you are delivering a solution they are actively seeking.

The revenue impact is tangible. Research indicates that advertisements informed by behavioral targeting can generate 2.7 times more revenue per ad than non-targeted campaigns. These initiatives consistently drive higher conversion rates, directly improving ROI. You can review more data in various studies on behavioral advertising performance.

Strengthen Client Retention with Proactive Advisories

Beyond new business acquisition, behavioral targeting is a powerful tool for client retention. By monitoring a current client’s digital behavior, you can identify emerging risks before they escalate into claims. This enables proactive engagement, building trust and solidifying your role as a strategic risk advisor.

Consider these practical applications:

- Proactive Risk Alerts: A client in the logistics sector begins researching new cross-border shipping regulations. This signal allows you to reach out with relevant risk mitigation advice and policy endorsements.

- Relevant Content Delivery: You observe a client is researching a specific industry challenge. You can then provide a targeted whitepaper or webinar invitation, reinforcing your expertise and value.

- Identifying Upsell Opportunities: A client shows interest in topics outside their current coverage, such as cyber liability. This provides a clear, data-backed opening to discuss expanding their policy.

This personalized, forward-thinking service model strengthens client relationships and makes them less susceptible to competitive pressures. It shifts the dynamic from a simple transaction to a strategic partnership.

Practical Applications for Insurance and Climate Risk

The real power of behavioral targeting is demonstrated in high-stakes industries like commercial insurance and climate risk. Here, it is an essential tool for anticipating challenges and mitigating real-world damages.

Consider a commercial real estate developer whose team begins researching coastal climate projections and hurricane-rated building materials. An insurer using behavioral targeting can identify this shift in focus. Instead of a generic ad, they can deliver content about specialized construction risk policies or engineering advisory services, transforming the ad into a timely solution.

This approach is equally effective for brokers. A broker researching new data breach trends can be presented with information on a new, highly specific cyber liability policy. The timing is precise, it demonstrates market awareness, and it directly addresses a risk that the broker is already considering for their clients.

Proactive Disaster Communications

One of the most powerful applications is in proactive disaster response. Historically, insurers sent broad, geography-based alerts ahead of a major storm. Behavioral targeting adds a crucial layer of intelligence.

By tracking regional search trends and online discussions, insurers can identify where public anxiety is highest. A sudden increase in searches for "business flood preparation" or "how to secure commercial property for high winds" in specific ZIP codes is a key indicator of imminent concern. This allows for the delivery of hyper-targeted communications—safety alerts, claim filing instructions, and risk checklists—to the policyholders who need them most. You can explore this further in our analysis of modern climate risk assessment tools.

This is not merely about sending another email. It is about using behavioral signals to deploy resources more effectively and demonstrate value during a crisis. It positions the insurer as a partner in resilience, not just a vendor.

Use Cases Across the Insurance Value Chain

The applications extend across the entire insurance lifecycle, delivering tangible value for different professional roles.

- For Underwriters: An underwriter observes a logistics company researching alternative shipping routes due to geopolitical instability. This insight provides far richer context for assessing their supply chain or cargo policies than a static application form.

- For Brokers: A broker can identify a segment of commercial clients showing interest in ESG (Environmental, Social, and Governance) reporting standards. This creates an ideal opportunity to share targeted information about D&O policies that cover new climate-related disclosure requirements.

- For Risk Managers: A carrier's risk manager can monitor behavioral trends to identify emerging industry-wide threats. A spike in research around a new industrial chemical could serve as an early warning for a future liability trend requiring closer examination.

These examples demonstrate how a deep understanding of what is behavioral targeting enables insurance professionals to shift from a reactive to a predictive posture. This is how you build stronger client relationships and a more resilient bottom line.

Navigating Data Privacy and Ethical Guidelines

A lock icon overlaid on a digital network, symbolizing data privacy and security.

A successful behavioral targeting program requires more than effective technology; it demands a rigorous commitment to ethical data handling. For decision-makers in the commercial insurance sector, this is not optional. It is essential for protecting brand reputation and avoiding significant legal and financial penalties.

While data is the engine of this strategy, regulators are closely scrutinizing how that data is collected, stored, and used. Regulations such as GDPR in Europe and CCPA in California have fundamentally altered the landscape, granting individuals greater control and placing a heavy burden of responsibility on businesses.

Building Trust Through Transparency

In the insurance industry, trust is the foundational asset. A transparent approach to data is not just good practice; it is the only sustainable strategy. This means replacing dense legal jargon with clear, comprehensible privacy policies.

A robust data management framework is non-negotiable. To ensure your targeting is both responsible and effective, you must adhere to essential data governance best practices. This structure enables the secure management of client data while maintaining compliance with evolving regulations.

The ultimate goal is not just compliance, but trustworthiness. When clients understand what data is being collected and why, they are more likely to view personalization as a valuable service rather than an intrusion.

Core Practices For Ethical Implementation

To put these principles into action, risk managers and underwriters must focus on three key areas. Mastering these ensures your strategy respects user privacy without sacrificing critical business insights.

- Implement Clear Consent Mechanisms: Users must actively opt-in to data collection. Avoid pre-checked boxes and ambiguous language. Consent should be granular, allowing individuals to choose precisely what they are comfortable sharing.

- Prioritize Data Anonymization: Whenever possible, remove personally identifiable information (PII). The goal of behavioral targeting is to identify patterns and trends, not track specific individuals. This step significantly reduces privacy risks.

- Maintain a Transparent Privacy Policy: Your policy must clearly state what data is collected and how it is used. For a practical example, you can review how we handle information in our own privacy policy.

By integrating these ethical guidelines into the foundation of your strategy, you create a system that not only drives growth but also strengthens the client relationships upon which your business is built.

Building Your Behavioral Targeting Strategy

Transitioning from understanding behavioral targeting to implementing it requires a structured plan. For insurance leaders, this is about creating a roadmap that achieves specific business goals—whether generating qualified leads for a new D&O policy or improving retention of high-value clients.

An effective strategy is built on clear objectives, intelligent segmentation, and the right technology stack.

First, define what success looks like. Are you aiming to increase market share in a new risk category? Or is the primary goal to cross-sell cyber liability policies to your existing commercial client base? Your objectives will guide every subsequent decision.

Creating a Phased Implementation Plan

The most effective way to integrate behavioral targeting is in managed stages. A "crawl, walk, run" approach minimizes initial risk and allows your team to build expertise.

- Crawl: Begin with your owned asset: first-party data. Analyze your website visitor behavior to identify high-intent prospects and build foundational audience segments.

- Walk: Layer in third-party data to enrich your profiles. Execute small-scale, targeted campaigns on a single channel, such as LinkedIn, to test messaging and measure initial results.

- Run: Once you have validated the approach, scale up to a multi-channel strategy. Implement advanced automation platforms to deliver personalized content across email, social media, and your website, creating a cohesive client journey.

This phased process is how you build a sustainable and scalable program. We detail this further in our guide to the lead generation process.

Start small to prove value early. A single successful pilot campaign, even if limited in scope, creates the momentum needed to justify a larger investment.

Finally, establish Key Performance Indicators (KPIs) to measure success. These might include cost per qualified lead, conversion rates on specific policy pages, or engagement with your risk advisory content.

With the behavioral targeting market projected to reach USD 29.8 billion by 2032, having the right KPIs in place is crucial for securing your share. You can explore more market insights at dataintelo.com. This framework provides executives with the tools to guide their teams toward an implementation that delivers measurable ROI.

Your Top Questions, Answered

For leaders in high-stakes industries like insurance and risk management, several critical questions arise regarding behavioral targeting. Here are direct answers to the most common inquiries.

Is Behavioral Targeting Just Another Name for Contextual Targeting?

No. They operate on fundamentally different principles.

Contextual targeting is about ad placement relative to content. For example, an ad for flood insurance appears next to an article about hurricane preparedness. The ad matches the *content* of the page.

Behavioral targeting is about the *individual*, not the page. It leverages a user’s digital history—the articles they have read, the searches they have conducted, and the products they have viewed. Therefore, the same flood insurance ad could appear on a financial news website because the user was researching flood maps a week prior.

In summary, contextual targeting focuses on the environment, while behavioral targeting focuses on the individual’s demonstrated intent.

How Does the End of Third-Party Cookies Impact This Strategy?

It does not end the strategy; it forces an evolution toward more transparent and durable methods. The deprecation of third-party cookies marks the end of an old, less transparent way of tracking, shifting the focus to consent-based data.

The new focus is on:

- First-Party Data: This is the new gold standard. It is data you collect directly from your own website visitors with their explicit consent, such as through newsletter sign-ups, quote requests, and content downloads.

- Privacy-First Technologies: New frameworks like Google's Privacy Sandbox are designed to group users into anonymous interest cohorts, enabling relevance without individual tracking.

- Authenticated Experiences: Companies are increasingly creating valuable, gated content or tools that encourage users to create an account, providing a direct, consensual channel for understanding their needs.

Can This Really Work for B2B Insurance?

Yes. It is arguably *more* powerful in the B2B insurance space.

B2B purchasing cycles are long, involve multiple decision-makers, and are driven by highly specific business challenges. Behavioral targeting allows you to bypass the noise and reach the right professional at the right company with a message that addresses a known pain point.

For example, you can deliver highly specific content about supply chain risk mitigation directly to a risk manager at a manufacturing firm who has spent the last month researching port closures and logistics delays. You are not guessing; you are responding to clear digital signals. This is about precision, not volume.

---

At Insurtech.bpcorp.eu, we convert climate-driven risks into validated business opportunities. Our Sentinel Shield platform provides real-time intelligence on businesses impacted by severe weather, enabling you to connect with high-intent prospects at their moment of need. Find your next opportunity at https://insurtech.bpcorp.eu.